Last time, we talked about Emergency Funds and learned how digital banks are a good way to store them. I already have a blog on GSave of GCash. But with the base interest rates of digital banks going down recently (Gsave from 3.1 to 2.6 percent since March 1), following the rise of inflation rate, I have been looking for another alternative and that’s what this blog is all about.

You probably read the title and thought, what’s a neobank and how is it different to a digital bank? Being a neobank means that it is a 100% digital bank. What about the others like CIMB and ING? Well, they either have a physical branch or an affiliation with a traditional bank. Digital banks and neobanks can offer higher interest rates compared to traditional banks as they have lesser operating expenses such as rent and manpower. Neobanks and digital banks are still PDIC insured up to ₱500,000 per investor.

So what are the features of Tonik?

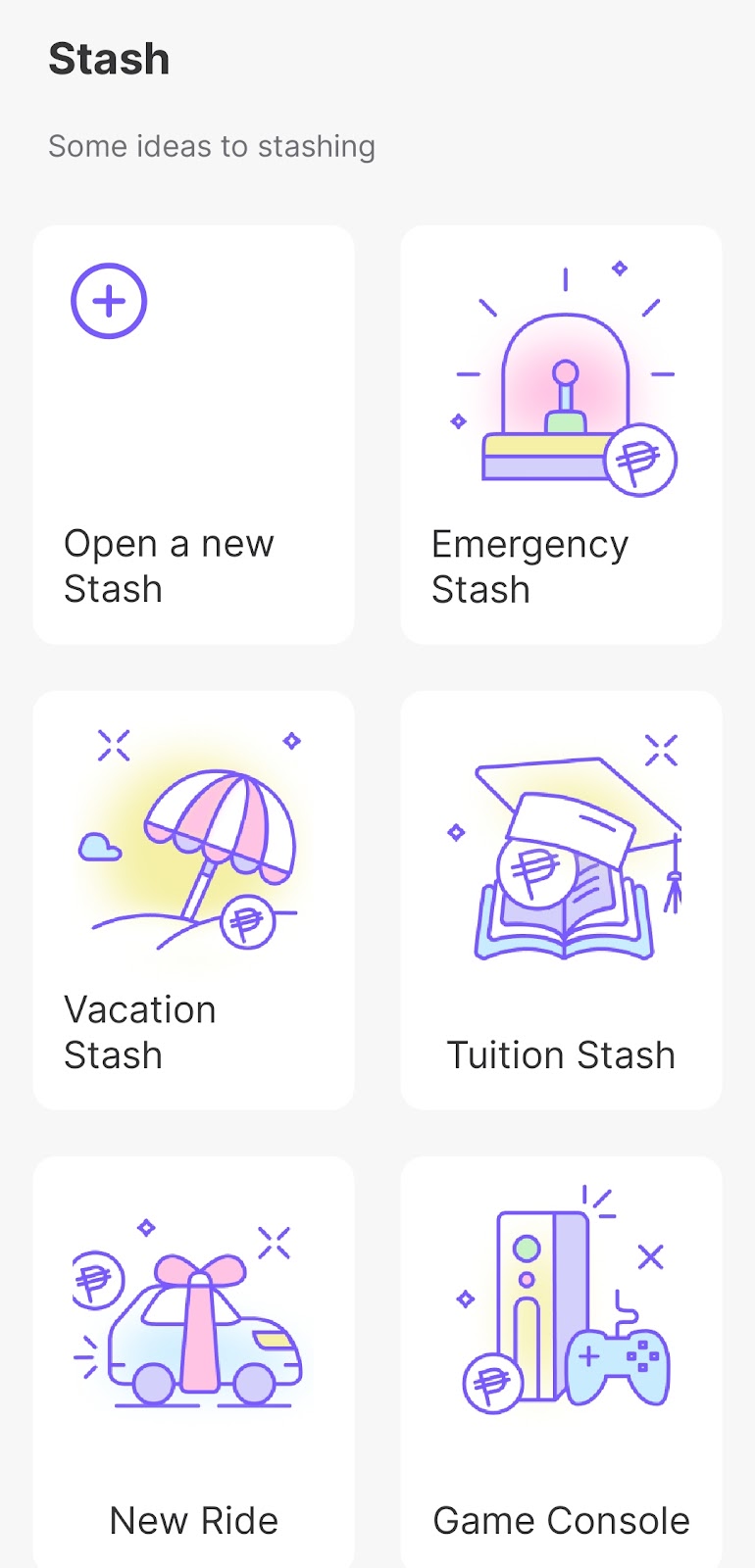

First one is stash, which is what we are familiar with. Stash is very liquid which means that you can add and remove funds instantly. There’s no maintaining balance and the interest rate is given per month, either on the first or last day of the month.

What I like about stash is that you can create different ones (up to 5) for different goals. You can even customize your own, so you won’t need to have a separate app/bank for different savings!

Types of Stash

There are two types of stash:

- Solo stash – this is more common as it’s for personal use. This will earn 4% interest per annum.

- Group stash – save with your friends and/or family. This is perfect for saving for a trip or a business. If you invite at least 2 members and all 3 of you contribute at least 1 peso, the interest rate will be increased to 4.5% per annum. Note that only the owner/creator of the stash can withdraw funds.

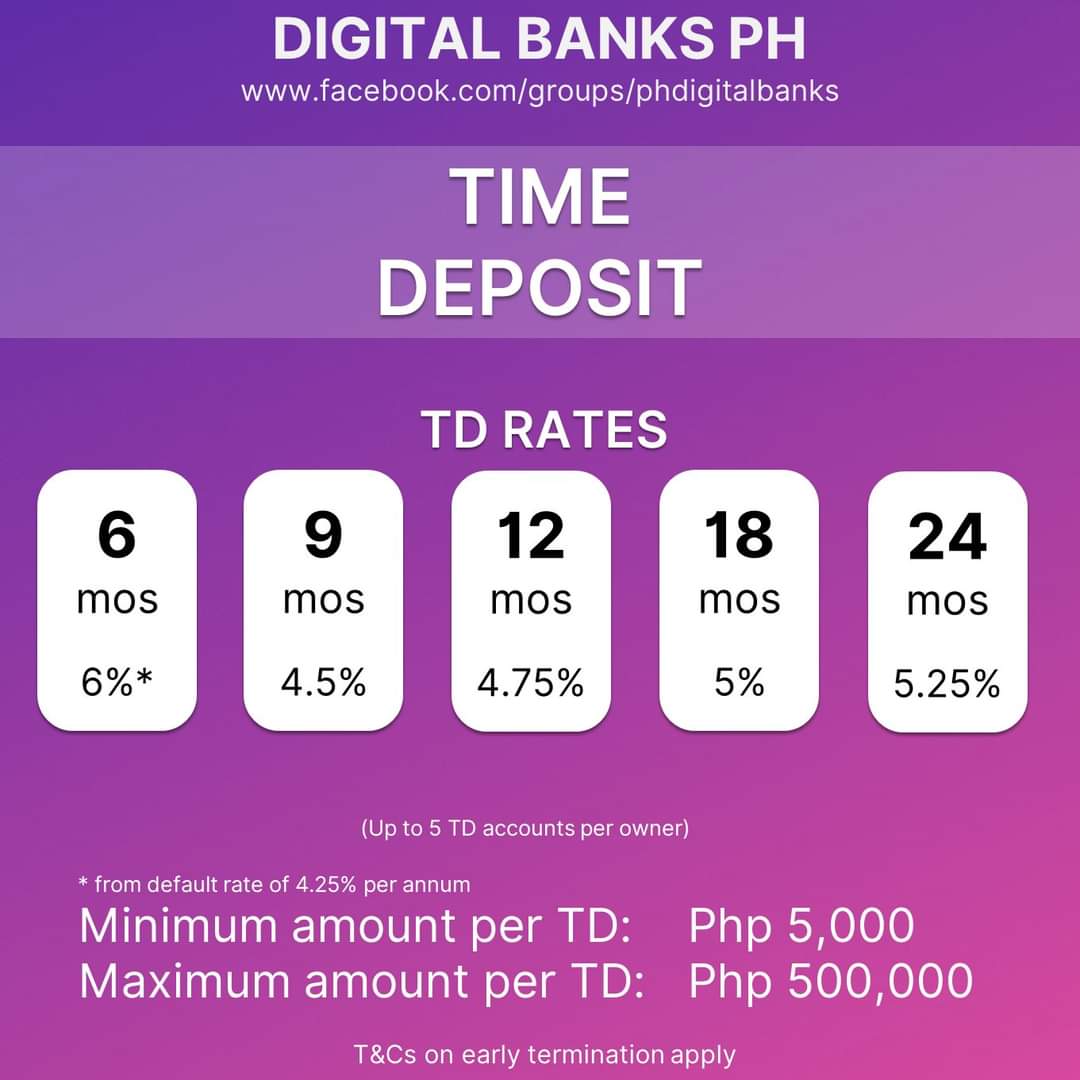

Time Deposit

The next feature which is unique to Tonik is Time Deposit (TD) . This acts like a normal time deposit that it will earn interest if you hold it for a specific time period, which means that there will be charges if you withdraw early.

The difference of this TD is that it gives higher yields than traditional banks since they’re all digital. Traditional banks right now only give at most 1% per annum, which is not enough to beat inflation rate which on average is 2-4%. The minimum time deposit amount is ₱5,000.

Tonik offers up to 6% per annum on TD. As seen in the picture, you’re probably thinking why is the 6% for 6 months, shouldn’t a longer time period have a higher interest rate? The reason is that the 6% is just a promotional rate to attract users as people tend to want a shorter holding period. I suggest maximizing this 6% rate while it’s still available, then just create a new one for another 6 months after it matures. Note that the rate may change anytime but your existing TD rate will not be affected.

The tricky part is the 6% per year but it’s only for 6 months. So the effective interest rate that you will receive for 6 months is just 3 percent. Note there’s still 20% withholding tax for the interest for both stash and TD. So the 6 months TD will give you a net of 2.4% interest.

You can create up to 5 TDs. Another difference of stash and TD is that you cannot add money to an existing TD. So make sure to only create a TD with the amount that you want to put.

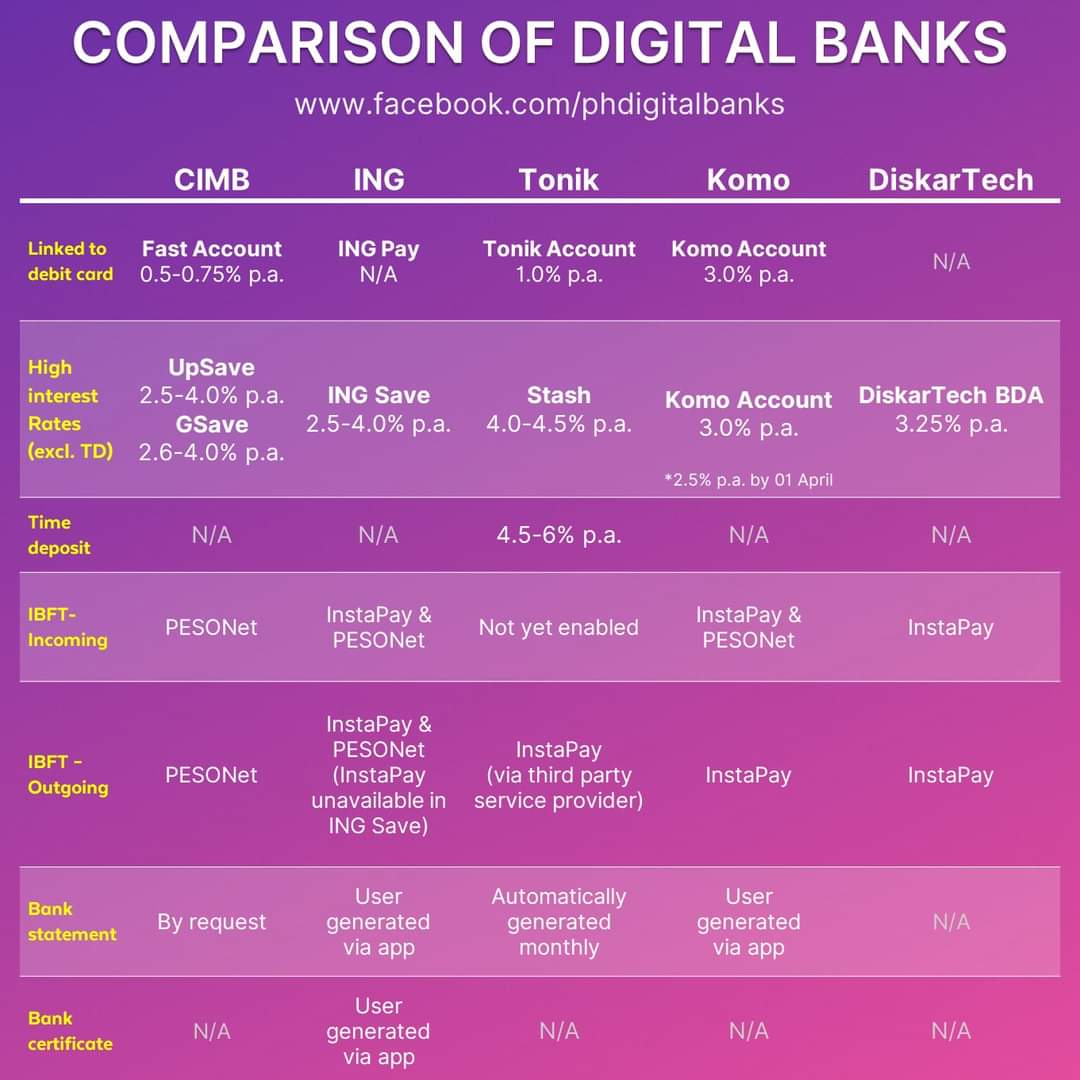

Tonik vs other digital banks

Here’s a breakdown of the differences of the digital banks in the Philippines:

Choosing what’s the best digital bank for you is very personal. But I suggest choosing the one that’s most convenient for you, since opening a new one will mean that you need to manage another account. You can use GSave/CIMB if you already have GCash and invest straight from the GCash app through GInvest.

Personally I have only used GSave/CIMB and Tonik. With CIMB only having PesoNet right now, where your transfer to other banks is not real time, I’m still leaving a small amount of my savings in my traditional bank. But with Tonik having Instapay where transfers are real time, I’ve transferred all my savings to GSave/CIMB and Tonik stash to maximize the interest rate since it’s very liquid and I can transfer anytime. UPDATE: you can check my blogs on other digital banks here.

We wouldn’t know until when these high interest rates will last for Tonik as most digital banks also started with the same rates. But the important thing is that you build the habit of saving consistently, so that your savings can at least match the inflation rate. I suggest trying it with a small amount first so that you get a feel for it then after a month you would receive an interest. Once you’re confident, you can now allocate a bigger portion so you can get higher interest.

How to start

Now that you know how Tonik works, how can you sign up? Registration takes less than 5 minutes. You just need to download the app in the Playstore or Appstore then input your mobile number. Then you’ll receive a One Time Password (OTP), then do a face scan along with validating your government ID. You can use my code TIGJXLY so we can both get P60 each. Then just fill in your personal details and password and you’re good to go! You can watch this for more details.

You can cash in online through these methods in real time. This is why I use GCash, as cash-in is done instantly for Tonik and other investments. Cash-out is also real time through GCash and Instapay to banks. Tonik automatically generates a bank statement every month. This is where you can see all your transactions for the month. Bank statements are needed for some investments and also when you’re applying for a Visa.

UPDATE: There will be charges cashing in to Tonik starting July 5, 2021.

If you have any issues on Tonik, you can reach out to their customer service through the help in the app. A better way is to chat with their Viber support as they’re more responsive, you just need to scan the QR code below

You can join the Tonik FB group. There’s also a separate FB group for discussing Digital banks in general. You can also watch Nicole Alba’s video on Tonik.

I hope you now have a better understanding on how Tonik and digital banks work. Feel free to share this to your friends and family. You can join the FB group that I created for additional learnings. You can also set up your free financial planning session with me so we can plan for your future.

“Do not save what is left after spending; instead spend what is left after saving.”

Warren Buffett