In finance, “emergency fund” is one of the most common terms that we hear or talk about. But what is an emergency fund and how much do we need to save for it?

Just a back story on why I’m writing this post, I started my own FB group about Financial Literacy just after my birthday last December 13. As of this writing, we’ve already grown to more than 5000 members just in the span of 2 months. I’m so blessed to have this platform that allows me to share finance tips and tricks to people of all ages all around the world. We have reached OFWs and even students, which is very exciting since they can start making good financial decisions at a young age.

In the past two months, I noticed that there was a lot of engagement in the group when it was a post about investments. But when it was a post about Emergency Funds and Insurance, it is more often than not, getting ignored. I’m writing this blog to shine a light on the mindset of the people.

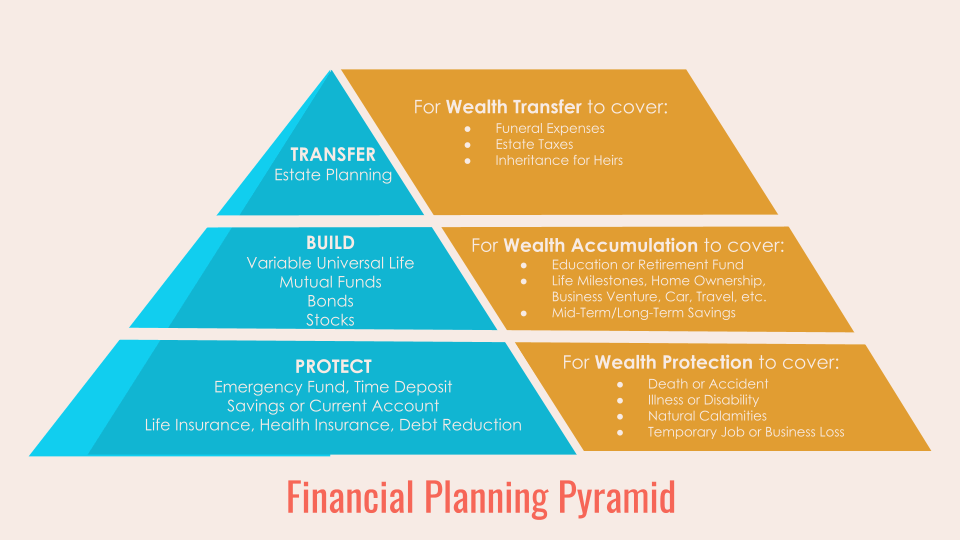

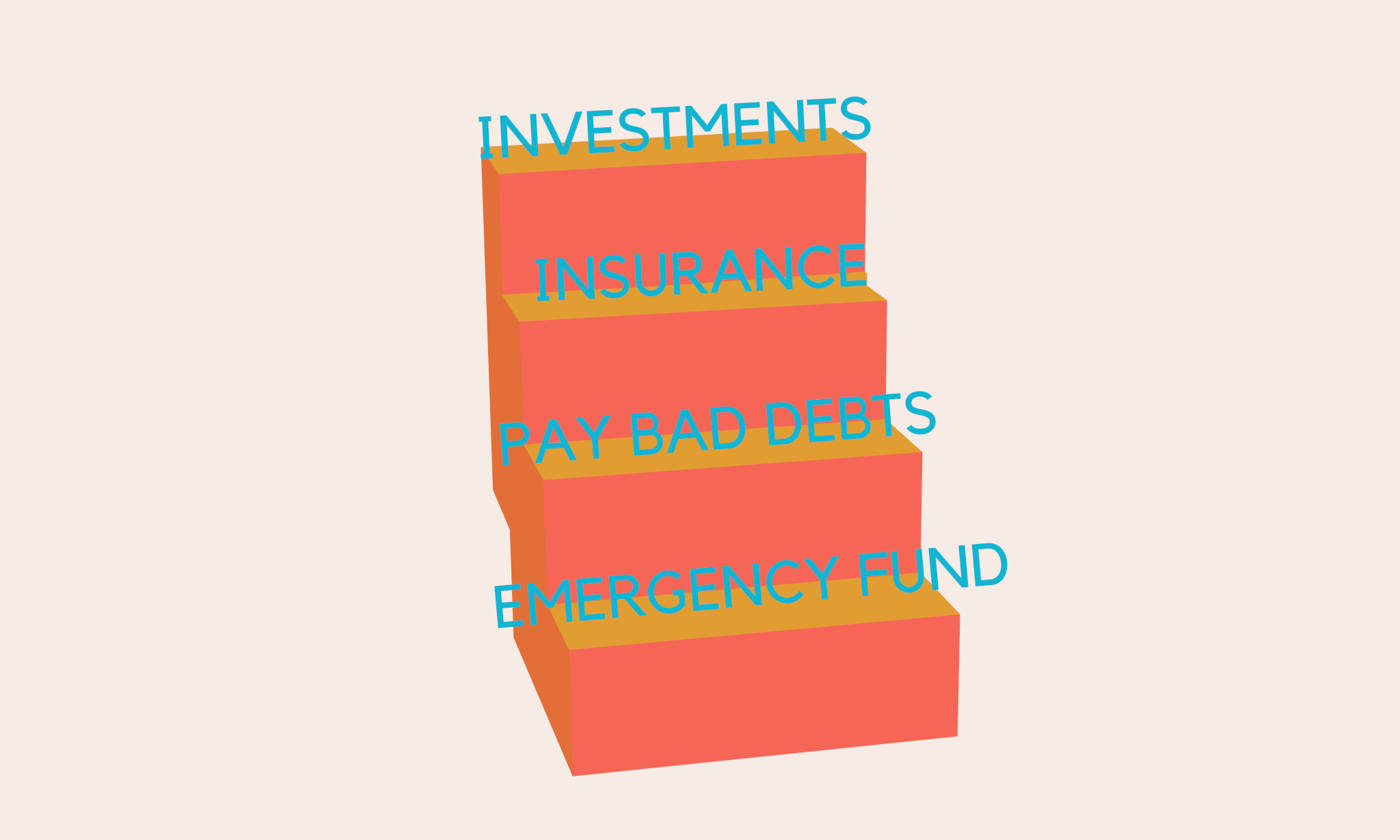

As you can see in our Financial Planning Pyramid, the foundation is Wealth Protection which covers Emergency Fund and Life/Health Insurance. We already know what insurance is for since I already have a blog for that, but what about an Emergency Fund?

Emergency Fund

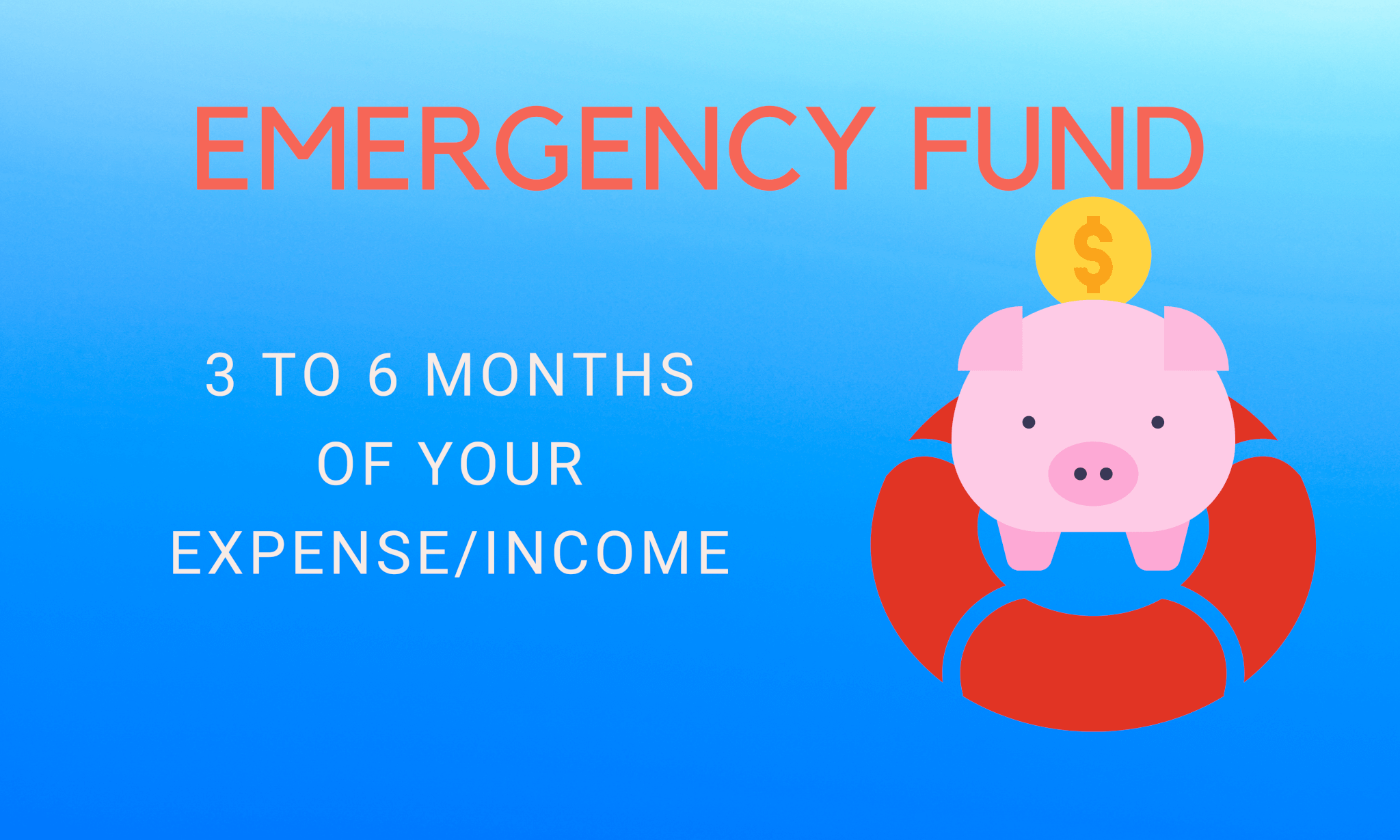

Emergency Fund (EF) is basically a fund that you have so that it can cover unexpected events like temporary job loss, medical bills, calamities such as this pandemic, and even home repairs etc. So how much do you need to save up for this? It varies from person to person but the rule of thumb is 3 to 6 months of your monthly expenses.

To get your monthly expenses, you should add all your fixed monthly expenses such as bills, subscriptions, insurance, grocery, online shopping etc. If we assume your monthly expense is ₱20,000, the EF that you need to build up is ₱60,000 – ₱120,000. This amount should be separate from your savings which will go towards your future goals.

“Nothing helps you sleep better at night than knowing that you have money tucked away for an emergency.”

Greg McBride

You can also use your monthly salary instead of your monthly expenses, if that works for you. No matter what you choose, your EF won’t be a fixed amount since you’ll encounter changes throughout your journey. Let’s say you have a family, then your EF should have a higher buffer (6 to 12 months) as you should factor in educational funds and daily expenses of your family. Having a sufficient EF is recommended as we are in this pandemic filled with uncertainty of when exactly will we be able to go back to living normal lives.

Where to store EF

A perfect way to store your Emergency Funds is through digital banks. Digital banks are good as they give returns (2.5% to 4% per annum) that can match inflation, which on average is around 3% per year. The interest of digital banks is given per month instead of per quarter in traditional banks. It’s also very liquid so you can withdraw anytime you need it. Real estate is not recommended for EF since even if the value appreciates over time, it will take some time to liquidate it. You can also check out other digital banks that I already wrote here.

Just note that once your EF is depleted, you need to build it up again. It might take a while to build it, but what’s important is that for every source of income you get, you should allocate a certain percentage or amount for your EF so that you can reach your target. You should also allocate a portion for savings and investments. Once you build up the habit of paying yourself first, you will know what to do with your money in the future.

Pay yourself first

We should fix the common practice that we have to spend when we get our income. No matter how big your income is, it’s still limited compared to your wants that can be unlimited. If you prioritize spending over saving, more or less you’ll have nothing to keep after paying everything, or even worse, you may get into debt since your income is not enough. We have to practice delayed gratification. Have a simple lifestyle so that you’re daily expenses are kept to a minimum. Save as much as you can and you can reap the benefits in the future.

The main reason as to why you need to start with building your EF, paying off your debts, and insurance first before investing is because you don’t want to have to withdraw your investments in case something happens.

Let’s say your investments, such as stocks, yield 10% interest. But then, something unexpected happens and since you don’t have an EF, you would need to withdraw your investments as soon as possible. This will likely cause a not so good return for you since it does not fit your timeline. If you had put ₱20,000 in the stock market hoping it would grow, but suddenly lost your job and don’t have an EF to pay your daily expenses, you would have no choice but to liquidate your stocks to pay for it. And there’s a high chance that at that moment, the market is down so you would’ve lost money.

Common questions

What if I already built my EF and I want to invest even if I don’t have enough capital yet, should I be taking a loan? The answer is quite tricky as the interest on your loans is fixed, while your returns on your investment are not. Unless you are sure that your investment is consistently giving a higher yield than the interest rate of your loan, then that’s the only time you should go for it. But always take precautions and remember that while investments have the power of compounding interests, debts have the same power too and we don’t want that. For me personally, I wouldn’t take that risk so that I can have the peace of mind that I’m debt free.

What about getting insurance even if I haven’t built my EF yet? It is not recommended as insurance is a big commitment. If you’re unable to pay your premium on time due to an emergency, there will be consequences such as your policy potentially lapsing, which means that all your contributions will be put to waste, you won’t be insured anymore, and you’ll go right back to square one.

What if I’m still living with my parents and I don’t really have any obligations or responsibilities yet, should I still build up my EF? If you are in this situation, that’s good for you! I suggest that you allot a small portion of your money for your EF just in case something comes up with your family so that you can help them out. This will be your headstart once you start paying the bills in the future.

Final thoughts

So the ideal order is to build your emergency fund first, pay bad debts (if you have any), get insurance, before getting into investments. Once you’re comfortable with the EF you have, maybe you’ve already built 3 months worth and you’re working hard on building the other 3 months, you can now also start investing so that you can grow your money even more.

Now that you know how to build up your emergency fund, let’s prioritize this before going into the big world of investments. We should not have the FOMO (fear of missing out) mentality when it comes to investments, no matter how profitable they may be, especially when you don’t understand what investments you’re going into.

Please share this with your friends and family so that we can shift their mindset. Do join and invite them to the FinLit FB Group for additional learnings.

The prudent sees danger and hides himself, but the simple go on and suffer for it.

Proverbs 27:12 (ESV)