We’ve all heard of the 7 wonders of the world, places we all want to travel to and visit as we’ve been stuck in our homes for almost 2 years now due to the pandemic. But have you heard of the 8th wonder of the world? Albert Einstein once described compound interest as the “8th wonder of the world, he who understands it, earns it; he who doesn’t, pays for it.”

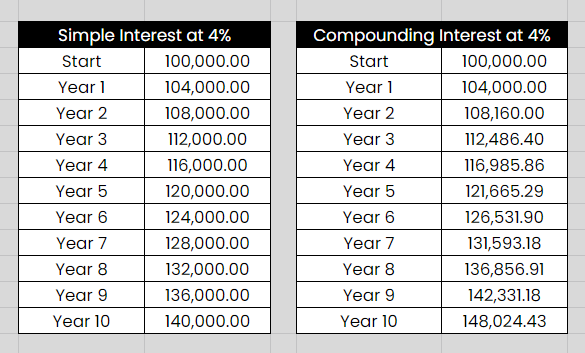

Basically, compounding interest means that your interest is also earning interest. In the table below, the comparison between a simple 4% interest versus a compounding 4% interest is shown.

As you can see, simple interest is based on the principal amount of the deposit. While compound interest is based on the principal amount and the interest that accumulates on top of it in every period. Simple interest is calculated only on the principal amount of a deposit, so it is easier to determine than compound interest

Compounding is so powerful that it can work for you or against you. I know I’ve already explained how it can work for you, but it can work against you when it comes to credit cards, loans and inflation.

Compounding Interest Working Against You

Remember when using a credit card, you need to pay the full amount due per month, not just the minimum balance (3 to 10% of total amount) as you’ll leave a balance that’s carried over to the next credit card billing cycle. In addition, the bank will charge you high interest on the overdue amount plus the outstanding balance, this is another example of compounding.

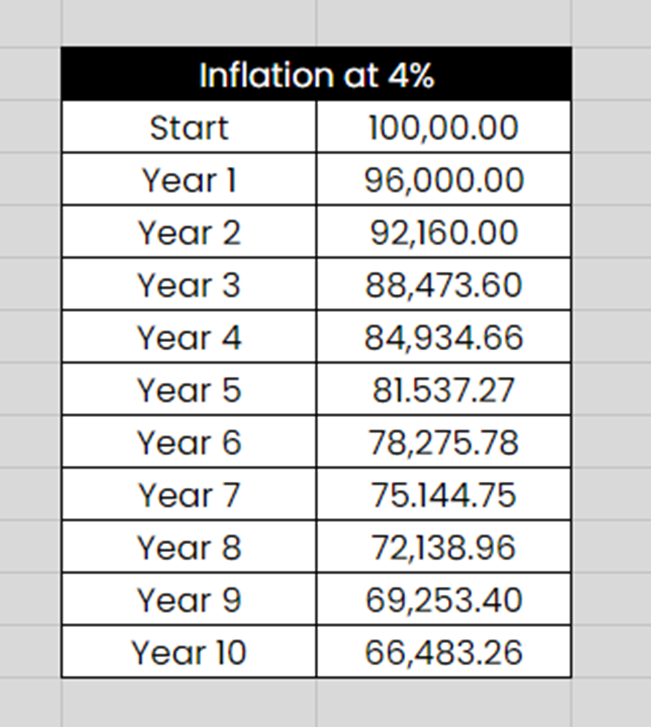

Inflation is the rate at which the value of a currency is falling and, consequently, the general level of prices for goods and services rises. The average inflation rate in the Philippines is at 4% per year.

Putting your money in a normal savings account is not a viable option at this point of time as it only earns a measly 0.125% per annum, not to mention the 20% withholding tax. You can see the huge difference of 0.125% vs the 4% inflation rate. So our main goal for us to reach our financial goals is to not just match inflation, but beat it as well. This can be done by putting our money in the right savings and investment vehicles.

Compounding Interest Working For You

Compounding Interest can work to your advantage if you use it to save and invest. Here are some examples:

- Digital banks such as Tonik and GSave, as long as you won’t withdraw as it employs monthly interest.

- MP2 upon withdrawing after 5 year maturity. You can also invest it as a lump sum after 5 years if you don’t need the money for it to compound for another 5 years.

- Dividend paying stocks with dividends reinvested. This is a good strategy to have passive income for life.

- Time deposit that you rollover. Tonik is an example with up to 6% per annum, the interest is 6% per year but it’s only for 6 months. So the effective interest rate that you will receive for 6 months is just 3 percent. You’ll need to rollover the capital and the interest again for another 6 months to get the full 6%. Note that there’s also a 20% withholding tax.

We can maximize compounding interest to our advantage by starting ASAP. We can just start small and be consistent putting a certain amount per month or when it’s convenient for us.

With this example, you can see the difference between investing with more time versus investing with more money: Investing ₱30,000 annually for 10 years and holding it for 30 years compared to Investing ₱60,000 annually for 25 years and holding it for 25 years.

Even if you invested a smaller amount, all in all, ₱300,000 compared to the ₱1,500,000, the value after inflation of the former is on par with the latter just because of time and compounding interest.

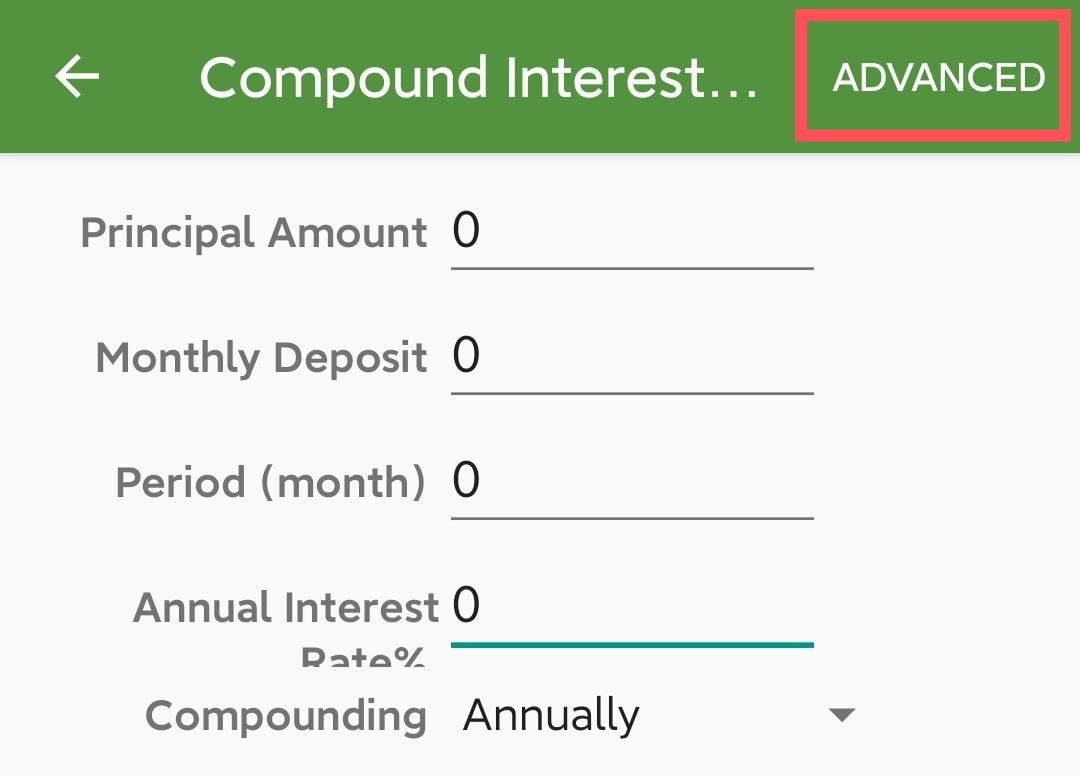

You can use this link for a sample compounding interest calculator. You can also download the app that I used in the Playstore or App Store. It’s under Compounding Interest then choose “Advanced” in the upper-right so you can also include the inflation rate.

Final Thoughts

When it comes to investing, instead of always looking for the investment vehicle that gives us the highest returns to the point of taking too much risk, we can still reach our goals by the power of compounding interest and a long time horizon.

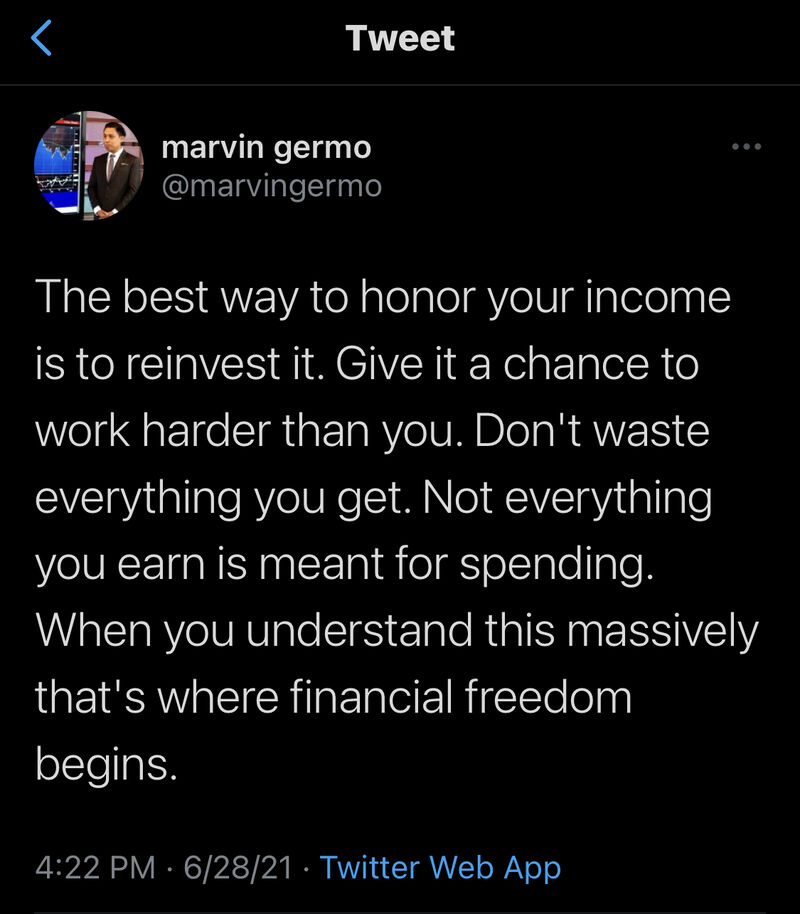

When your business/investments are going well, the best practice is to not withdraw your earnings, we can maximize the power of compounding interest by reinvesting everything and adding more frequently. We should earn and save/invest as much as possible, let money work hard for us and one day it’ll all pay off.

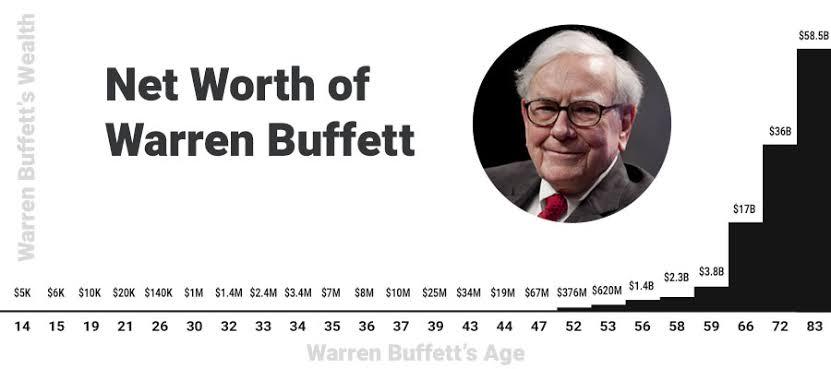

Warren Buffet, one of the greatest investors is a perfect example of how compounding interest works wonders to his net worth. 99% of his immense wealth was earned after his 50th birthday. He started his financial path toward wealth at a very young age and built his fortune slowly over the years. We might not get to billionaire status in our lifetime, but we can all start with what we have right now and reach our 1st million and other goals one step at a time.

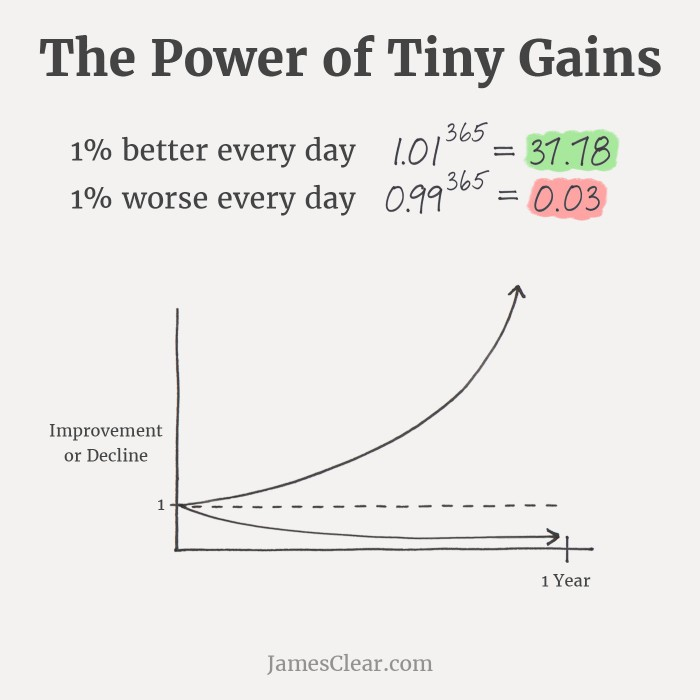

Compounding doesn’t only happen in money, it also works when improving oneself so let’s aim to be at least 1% better each day.